If your business is built around providing physical merchandise or products to customers, you know how important it is to always have enough inventory on hand to meet demand. However, as operational costs pile up, investments in areas like marketing, R&D, or sales might suddenly dominate your budget in one month or quarter. As a result, you may find that maintaining enough capital to always afford sufficient stock is harder than it sounds. This is where inventory financing comes into play.

Context: Needing Inventory but Lacking Capital

If your small business is built around providing physical merchandise or products to customers, you know how important it is to always have enough inventory on hand to meet demand.

To business owners first starting out, this seems like a no-brainer. If inventory is the lifeblood of the organization (and what ultimately drives revenue), then of course restocking the shelves as sales occur will be a top priority. However, as operational costs pile up, investments in areas like marketing, R&D, or sales might suddenly dominate your budget in one month or quarter. As a result, you may find that maintaining enough capital to always afford sufficient stock is harder than it sounds.

But while a lack of capital might force unstable businesses to become ultra selective of which investments they pursue, companies with a proven track record of success need not be so selective. This is true even if such businesses still experience liquidity shortages from time-to-time.

How so, you might ask?

If your business is experiencing sustained growth, there are a broad range of options available for financing the various elements of your expansion. Today, financing is available for everything from equipment, personnel, and real estate to inventory and raw materials. Ultimately, accessing this financing ensures that small but established businesses in need of additional capital can continue supporting daily operations (i.e. purchasing more inventory) while also pursuing ventures that help them stay ahead of the competition (i.e. deploying new marketing or sales campaigns).

To better understand how business financing can enable this type of growth, let’s narrow our focus to one specific type—inventory financing.

What is Inventory Financing?

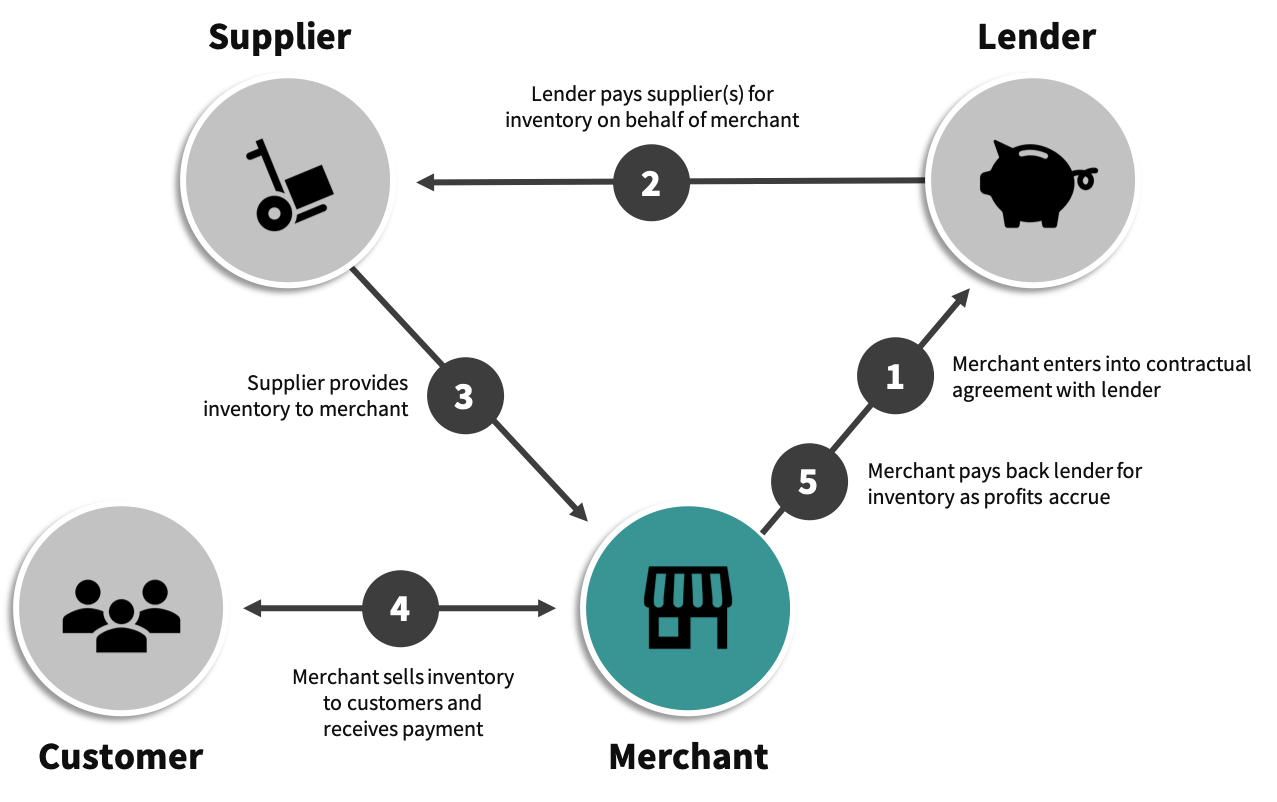

Inventory financing is exactly what it sounds like; a company (lender) gives you access to funds that you use to purchase inventory, and then you pay the lender back as your inventory is sold for a profit. At its core, inventory financing is a debt-based funding solution—a type of business loan—that provides you with the cash necessary for purchasing inventory that is needed to meet demand.

With inventory financing, you can only use the funds you acquire to purchase—you guessed it—inventory. You’ll receive the exact amount of capital you need to purchase an order—nothing more, nothing less—for the exclusive purpose of replenishing your stock.

As business loan options go, inventory financing is uniquely strategic for a few reasons. But before we delve too far into the value-add, let’s take a closer look at how it works.

How Inventory Financing Works

Why is Inventory Financing Necessary & What are the Parameters?

As an operator for (or owner of) any business that sells physical products, you can probably think of a few situations where it would be nice to have more cash on hand to buy inventory. Perhaps you’re gearing up to expand sales at your brick-and-mortar location(s) and need financing to stock the shelves. Or, maybe one of your suppliers is offering a temporary sale on one of your top-performing products, which could mean massive savings if you are able to quickly buy in bulk. Or even still (as has been highlighted in recent news coverage), perhaps the inventory you purchase from overseas suppliers is about to be impacted by rising tariffs, and you want to order a large quantity of product in advance of these tariffs to avoid the impending upcharges.

Regardless of whether the above examples apply to you, the point is that many businesses will sooner or later find themselves in need of assistance to purchase additional inventory. Inventory financing is ideal in these scenarios for two reasons. For one, choosing NOT to expand inventory levels can create scenarios where backorders and stock-outs become a recurring theme. This can lead to missed sales opportunities and serious customer satisfaction problems. But alternatively, purchasing too much inventory on your own (i.e. without a loan) that doesn’t sell and sits collecting dust on shelves can significantly hinder your cash flow (and remember, 82% of businesses reportedly fail because of cash flow problems).

Considering the above dilemmas, inventory financing is advantageous because it acts as a “self-secured” loan. This means you don’t need to put up additional collateral when receiving funds—the inventory itself acts as the collateral. Of course, this will require your lender to perform its due diligence and make sure that, in the event that you default on your loan payments, they can recoup the inventory and sell it on their own to make back profits. That being the case, you probably won’t get an inventory financing loan for highly perishable items like shrimp or produce. (Twinkies should be fine.)

Looking beyond the above criteria, there are several other requirements you’ll typically have to meet in order to qualify for inventory financing, including:

At least one year of business history: Brand new start-ups need not apply here—lenders want to see that you have a history of profitability and sustainability.

Minimum lender requirements: Every lender is different, but many won’t want to extend you financing for less than a certain amount of capital (in some cases the minimum is $500,000). For loans of lesser amounts, a general business line of credit is recommended instead.

Detailed financial records: Most good lenders will want to see financial records that show your sales volumes, inventory turnover rate, and gross profit margins, among other reports. Quality accounting software that can generate these reports quickly and accurately is recommended.

What is Required to Access Inventory Financing?

If your company can meet these specifications, inventory financing could be a highly effective avenue for supporting your expansion and ensuring that you don’t deplete your working capital as you grow.

Five Ways Inventory Financing Helps Small Businesses Grow

For further insight on some of the various ways that inventory financing can be strategically deployed, consider the five following scenarios.

1. Jumpstart Sales Across New Markets or Channels

In theory, having to accommodate growing demand for your business is a good thing. However, to capitalize on this heightened demand, your business needs to have enough product available to sell. But without adequate funding, you can’t buy more inventory. And without more inventory, you can’t generate the sales you need to grow. It’s a catch-22 business problem that many small companies face today.

To address the problem, you could pillage your rainy day fund to make a big upfront purchase of inventory. But, that will leave you exposed in the case of an emergency. And while paying for your inventory is important, you can’t sacrifice your investments in things like payroll or rent either.

With inventory financing, you can support the required buildout of inventory without draining your cash reserves. This additional inventory can be used for selling to customers:

In a new market (i.e. a new geographic region),

In a new industry segment (via a new type of product or portfolio of products ), or

Through new sales channels (i.e. jumpstarting a direct-to-consumer channel via an e-commerce site).

In any case, using an inventory loan to boost your stock allows you to service more customers without exasperating your own limited funds. And ultimately, you can pay your lender back with the money you make from the additional sales volume.

2. Take Advantage of Seasonal Spikes in Demand

Perhaps your business isn’t looking to expand, but just to take advantage of seasonal spikes in business. The best example of this is the winter holiday season; It can be a goldmine for small businesses, provided you have enough inventory on hand to meet demand.

With inventory financing, you can stockpile inventory ahead of an expected boom and use your additional revenue to pay off your interest payments (and then some).

Furthermore, it’s worth noting that the best time to buy seasonal inventory is often during the offseason (think about the huge discounts on Christmas decorations that are offered in January). As such, the best time to reorder inventory (to capitalize on lower price points) is during periods of low demand. However, this is also likely when your sales are lagging, which means that purchasing goods during this time, even at a discounted rate, can be a drain on your cash flow.

In order to cost-effectively deliver orders to customers at a speed that competes with big businesses, you may need to store inventory at multiple distribution centers (beyond just your primary office or warehouse). For instance, if you have a large customer base on both the East and West coast, storing inventory at facilities in Virginia and Nevada ensures all these customers get 1-2-day delivery when they purchase your products.

To achieve this level of efficiency, you’ll need to make sure these additional facilities are adequately stocked, which may require you to maintain more inventory than you’re used to. In this circumstance, an inventory loan gives you the funds necessary to fill those warehouse shelves so that you can optimize the delivery process for all your customers.

4. Avoid Having to List Other Business Assets as Collateral

As mentioned earlier, one of the reasons inventory financing can be a good option for small businesses is that the inventory acts as collateral on the loan. In other words, you don’t have to put down any additional assets to be seized in the case of a default.

The advantages here are twofold. For one, if you own a small business, the reality is that you won’t have the kind of assets and collateral that larger organizations use to acquire affordable financing. Whereas most large enterprises can post millions (if not billions) of dollars worth of collateral to unlock financing as-needed, your small business’s assets may be worth much less. And without the leverage that a large asset base gives you, many traditional forms of financing may fall outside of your grasp. However, using a self-secured inventory financing loan ensures that a lack of additional collateral does not impact your chances of being approved.

Secondly, for small businesses that decide to leverage an alternative form of financing (such as a term loan), it may be that a majority (or at least a significant portion) of your business’s assets must be listed as collateral. This means that in the event of a default, you may lose control of some or all of your assets to the lender. To avoid this risk, using a self-secured loan like inventory financing ultimately means you’re better protected from a liability standpoint.

5. Maintain Flexibility to Access Other Forms of Financing

Depending on your business’s scenario, it may be that numerous forms of financing are being leveraged at once (e.g. a general line of credit, inventory financing, corporate credit cards, etc.). That’s because having unique financing products that are tailored to specific business functions can be beneficial. For instance, we’ve already discussed how inventory financing works well for purchasing inventory. But if you need a more flexible form of financing for working capital needs, a general business line of credit is a better bet.

Here’s why, then, inventory financing is such a strategic choice: because it’s a self-secured loan, it usually doesn’t impact your business credit report. This means you have broader flexibility to access other forms of financing while the loan is outstanding. If you’re a small business with a limited cash flow, a non-secured loan of an equivalent size could negatively impact your debt-to-income ratio. That ratio is one of many factors that lenders consider when deciding if you’re qualified for a term loan or line of credit. So, if you expect that you’ll need access to other sources of financing in the near future, using self-secured inventory financing might be the best path forward.

Final Thoughts: The Bottom Line on Inventory Financing

Regardless of the specific use case or scenario, the reality today is that there are numerous small businesses that need to increase their inventory capacity to support growth. But because the costs of acquiring additional inventory can be high, it can be tough for small business owners to fork over the cash without breaking the bank or risking their company’s financial well-being. That’s where inventory financing can help.

Through inventory financing, you can strategically grow your business by offering faster delivery times, entering new geographic regions or market verticals, and preparing for seasonal spikes in demand—all without having to put down any personal collateral.

They say, “You need to spend money to make money.” But if you don’t have money to spend, strategic inventory financing makes sure your growth opportunities aren’t limited. For more information about how inventory financing can benefit your business, contact Ware2Go or Fundera.

Our Newsletter

Get our latest insights on how to make your supply chain your competitive advantage

A UPS Company

Let Us Show You

We grow your business by getting you closer to your customers with guaranteed 2-day delivery. Flexible. Scalable. On-Demand.

Join our email list and receive monthly updates, industry insights and curated content. Don't miss out!